Welcome to the ultimate guide on mastering how to create a budget – because let’s face it, managing your money is the adulting Olympics we all secretly signed up for.

In this blog post, we’ll unravel the mysteries of budgeting. From deciphering your income like a financial Sherlock to battling debt with the gusto of a debt-slaying superhero, we’ve got your back. So, grab your financial cape and a cup of coffee – or maybe make it a double espresso – because we’re about to embark on a budgeting journey!

We’re diving into the art of budgeting! From unraveling the mysteries of income evaluation to masterfully categorizing expenses, we’ve got your back on the road to financial wisdom.

Explore the intricacies of emergency savings, dance with employer-matched retirement plans, and embrace the snowball strategy for debt like a financial maestro.

We’ll also venture into the realms of personal savings, retirement planning, and the undeniable importance of maintaining a budget.

Get ready for a rollercoaster of insights, practical tips on tracking progress, and the lowdown on why having a budget is crucial. This blog post isn’t just about numbers; it’s about empowering you to make savvy financial decisions with flair and finesse.

What Is A Budget?

You may be wondering, what even is a budget? It’s something that is talked about a lot but not often explained. According to Nerd Wallet, a budget is a plan on how you will spend your money based on how much money you expect to make and how many expenses you have.

How To Create A Budget?

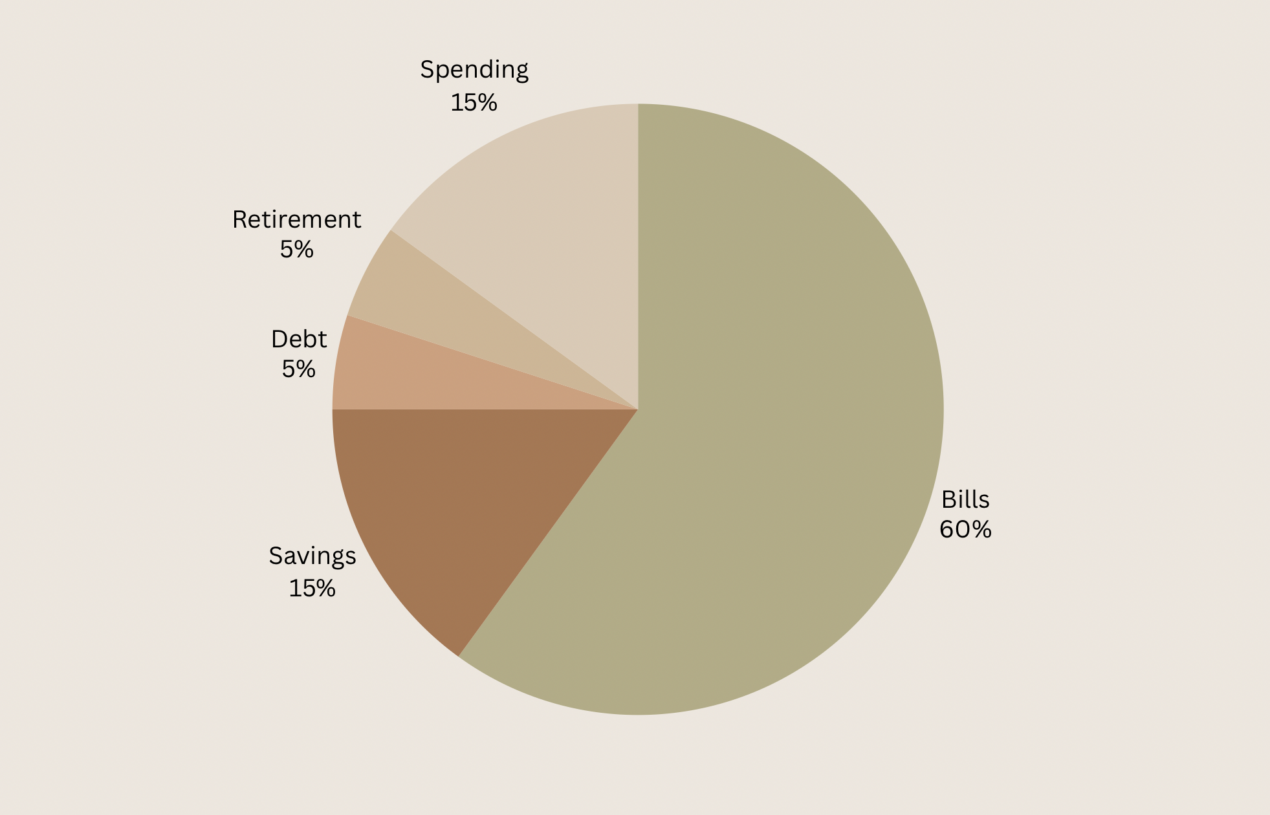

To create a budget, you need to start by compiling information on your income, your expenses, your debt, and your savings needs.

Below is a step-by-step guide to figuring out all of this information.

1. What Is Your Net Income or After-Tax Income?

The first and most important step is figuring out how much money you are making in total after taxes. When coming up with your budget, it may be easiest to determine this every month.

If you have paystubs, you can add together your last 6 months of paystubs and then divide by 6 to determine your average monthly income. If you don’t have pay stubs, you can check your monthly bank statements and do the same thing with 6 months of statements.

2. Create A List Of All Of Your Expenses

Once you’ve determined your monthly income, you will need to list out all of your expenses each month. The best way to do this is by taking a look at your monthly bank statements and pulling out your necessities such as bills, groceries, and transportation costs. If you have any bills that you pay intermittently such as annually or quarterly, make sure to divide those up to a monthly charge.

After you have a total of the expenses you have to pay each month, subtract that amount from your monthly income. This residual amount will be what we use to pay off debt, save, and for any other spending.

If you find that you don’t have enough to cover all of your expenses or you barely have anything left over afterward, it may be best to see if there are any areas where you can cut spending. A few common areas are utilities (Can you use your AC or heater less? Are you turning all the lights off in your house when you can? Are you using more water than you need to?), insurance (Can you pay less somewhere else?), subscriptions (Can you cancel any subscriptions you don’t use or need anymore?), mortgage (Are you able to refinance?), groceries (Are you buying any unhealthy items you could hold off on? Could you buy the generic version? Is your grocery store too expensive?).

Really scrutinize what you’re spending and see if there are any areas where you can save money.

3. Emergency Savings

This is something I’d never even heard of until I was older. Emergency savings can help with all of those surprise purchases that come up such as a flat tire, a parking ticket, or even a broken tooth!

It is recommended that you save between 3-6 months of your living expenses for your emergency savings. The reason for this is if something happens to you or you lose your job, you would have a 3-6 months cushion to figure out what to do next.

I believe that most people don’t maintain an emergency savings that large, especially in today’s economy. It is good to have a goal of that amount and always be working towards it. Just making sure that you are putting a little aside for emergencies is enough though.

4. Employer Matched Retirement Savings

The next important savings bucket is putting in enough to receive your employer-matched retirement savings. This is essentially free money you are getting from your employer and you don’t want to miss out on it.

Contact your HR Representative and find out if your employer offers a match, how much it is, and what is required of you to receive it.

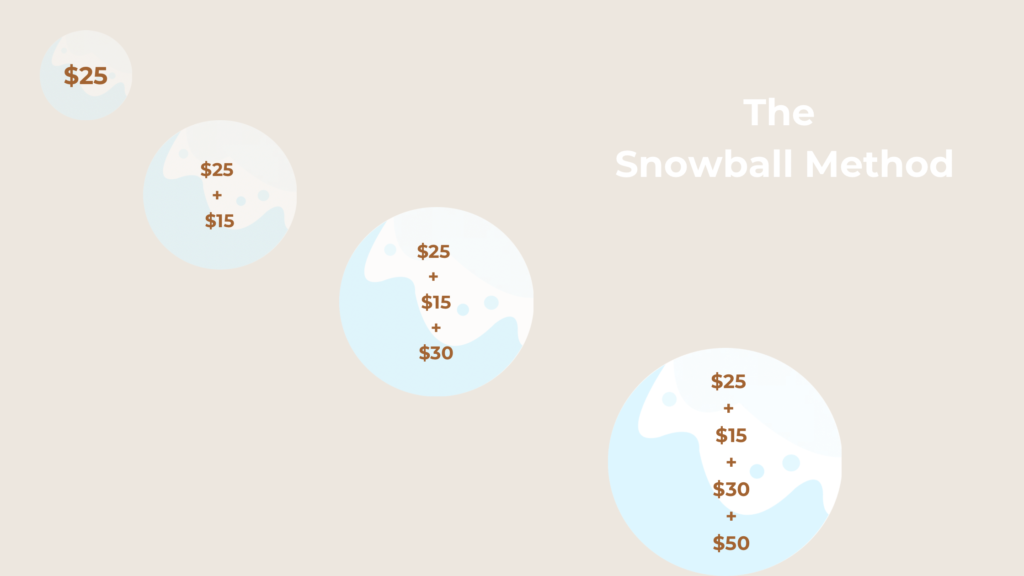

5. Paying Down Debt

It seems that almost everyone has some kind of debt nowadays. Of course, we don’t want this to start piling up so you need to determine what you can pay towards it. The amount you should pay depends on how much debt you have.

If you don’t have any bad debt such as large credit card balances or personal loans, then if you can you should pay off your credit cards each month to avoid interest.

If you do have bad debt, I recommend using one of the many debt repayment calculators to determine how much extra you should be paying depending on how quickly you want your debt paid down.

I personally use the snowball method which involves paying extra towards one card at a time- either one with the highest balance or the one with the highest APR and as you pay each card off, you apply the amount you were previously paying towards the next card.

6. Retirement Savings

Not everyone saves for retirement. I’ve heard a lot of people say that they will work until they die. I feel that this is unrealistic to a certain extent. Once you are ready to retire from your normal job, you can volunteer places or work an easier job that doesn’t make as much or involve as much brain power or physical labor. You need to be prepared for this time in your life.

The concept of saving for retirement can seem daunting and you may put it off thinking you’ll start when you get older. The younger you are when you start, the more you’ll have later on and the less you’ll need to save as you get older.

How much you should save and where you should be saving will be different for each person. I recommend doing your research and determining what is best for you.

7. Personal Savings

Now that we’ve got all of the big things out of the way, it’s time to save for yourself! You may be saving to buy a house, buy a new car, or go on a nice vacation.

Whatever it is you are saving for, decide how long until you would like to realistically hit that goal and divide the amount by the months you have until then. That is how much you’ll want to put into that savings.

You may not have enough to put towards that goal, if that is the case, you’ll need to adjust your timeline to something more achievable.

8. Spending Money

Good news! If you have extra money after you’ve completed steps 1-7, you have some money to spend on you or your family! Be responsible with this money, don’t spend it all in one place. But have fun! You deserve it.

How To Stick To Your Budget

Sticking to your budget is probably the most difficult part of creating a budget. You’re going to be tempted to purchase things you want on a whim but don’t! There are a few tricks to ensuring that you don’t spend outside of your budget.

Track Progress

It can be really rewarding to see all the money you’ve saved. Take time to look through your savings and be proud of what you’ve accomplished.

You can track this in an Excel spreadsheet, software like Quicken Simplifi, or Notion like me.

Automate What You Can

Something that I do that has really helped me is I have my savings automatically come out of my paycheck. That way you don’t even register that you have that money. I have a separate high-yield savings account where the money I save is transferred each month.

Why Having A Budget Is Important

I’m sure that some of you are reading this thinking that you don’t need to create a budget. Here is why that is not true: having a budget ensures that you are hitting your goals whether that be savings goals, retirement goals, paying off debt, or simply reducing your overall spending. We all have financial goals and setting yourself up to achieve those is such a rewarding process.

Having a budget will not only help you achieve your goals, it can show you where you can improve your finances. Whether you think you should be making more money or spending less, you can determine the best route by tracking your finances and sticking to a budget.

FAQ Section

There are so many different rules out there that people swear by. What you decide to use is up to you. You may have heard of the two below:

50/30/20: where you split your after-tax income 50% towards needs, 30% towards wants, and 20% towards savings. Depending on your goals, this could be the right path for you.

70/20/10: where you split your after-tax income 70% towards your living expenses, 20% towards repaying debt or your savings if you have no debt, and 10% would be your spending money to use as you please. This could be good for you if you have higher expenses and don’t feel that you need to spend as much on yourself.*

These rules are not universal so you need to assess your goals and overall expenses and determine if you’d want to incorporate a rule into your budget.

If I had to pick one thing that I think everyone needs to do when budgeting, it would be having some sort of accountability. Whether that is you tracking your spending and savings or a partner or loved one monitoring it for you. Having accountability helps us stay on track.

I believe that the hardest part of budgeting is sticking to the budget. Do whatever you can to make it easy for you to not overspend. One good trick would be taking out cash for each budget and putting it in envelopes and not using your debit card.

Using Google Sheets

Start by opening a new spreadsheet and labeling columns for income and expenses.

List all sources of income and categorize your expenses, such as housing, utilities, groceries, and entertainment.

Utilize the SUM function to automatically calculate totals for each category, providing a clear overview of your financial picture.

Using Excel

Begin by opening a new Excel workbook and creating labeled columns for income and expenditures.

Detail your income sources and categorize your expenses, such as bills, groceries, and entertainment.

Leverage Excel’s SUM function to automatically calculate totals, giving you a clear snapshot of your financial landscape.

Utilize formatting features to enhance clarity and make your spreadsheet visually appealing.

Using Numbers

Begin by launching Numbers and opening a new spreadsheet.

Designate columns for income and expenses, categorizing your various financial aspects.

Input your income sources and break down expenses into categories such as bills, groceries, and entertainment.

Leverage Numbers’ user-friendly interface to easily format and customize your spreadsheet.

Use the SUM function to automatically calculate totals for each category, offering a comprehensive overview of your finances.

Numbers also allows for easy integration of charts and graphs to visualize your budget trends.

Using Notion

Start by creating a new page in Notion and designating tables for income and expenses.

Break down your income sources and categorize your expenditures, including bills, groceries, and discretionary spending.

Notion’s flexible database features allow you to customize your budget structure to suit your preferences. Utilize the roll-up and relation properties to automatically calculate totals and create dynamic connections between different aspects of your budget.

The versatile nature of Notion enables you to incorporate additional information, such as due dates or notes, for a more comprehensive overview.

Budgeting when you don’t have a regular income requires a flexible and proactive approach.

Begin by assessing your average monthly income over a longer timeframe, considering fluctuations and seasonal variations. Prioritize essential expenses like rent, utilities, and groceries, allocating a portion of your income to cover these necessities.

Create a contingency fund to handle unpredictable expenses or income gaps. Embrace a minimalist lifestyle and distinguish between needs and wants, focusing on essential expenditures.

Consider diversifying income streams with side gigs or freelance work to enhance financial stability. Track and adjust your budget regularly, adapting to changes in your income.

Embracing a proactive and adaptable mindset is key when budgeting without a consistent income, allowing you to navigate financial uncertainties more effectively.

Harnessing the power of ChatGPT to create a budget involves crafting a clear and detailed prompt.

For example, you can input a prompt like, “Assist me in creating a monthly budget by providing insights on categorizing expenses, setting realistic limits, and optimizing spending habits. Consider variations in income and offer tips on maintaining financial flexibility. Additionally, suggest ways to track expenses effectively and any tools or strategies that may aid in budget adherence. Please provide a comprehensive guide tailored to my individual financial situation.”

By engaging ChatGPT with a thoughtful and specific prompt, you can receive personalized advice and insights to streamline the budgeting process and achieve your financial goals.

In wrapping up our financial escapade, you’ve now journeyed through the budgeting maze armed with wit and wisdom.

We began by demystifying the budget – that elusive creature often talked about but rarely explained. From decoding your income like a financial detective to creating a spreadsheet that would make any accountant proud, you’ve grasped the art of budgeting.

Navigating through emergency savings, employer-matched retirement plans, and the strategic snowball dance with debt, you’ve acquired tools for fiscal prowess. Armed with tips on tracking progress and automating savings, you’re now poised to conquer your financial goals.

If you found this post helpful, leave a comment with what other topics you’d like me to write about!